In 2026, the UK vaping industry is entering a completely new phase. This is not a ban or a simple regulatory update – it is the formal implementation of an excise duty system combined with physical duty stamps.

In 2026, the UK vaping industry is entering a completely new phase. This is not a ban or a simple regulatory update – it is the formal implementation of an excise duty system combined with physical duty stamps.

Led by HM Revenue & Customs (HMRC), the Vaping Products Duty (VPD) and the accompanying Vaping Duty Stamps (VDS) scheme opened for applications on 1 April 2026. This marks the shift from “planning stage” to “implementation stage” – the industry is now entering the real operational phase.

For brands planning their UK market entry, understanding the rules, identifying your obligations, and preparing application documents in advance are critical tasks to complete over the next six months.

1. First things first: What exactly is being taxed?

This is the most common point of confusion. Many people assume the UK is starting to tax vaping “devices”. That is not accurate.

The VPD is not based on the device itself, but on the volume of e-liquid (ml). In other words, the taxable unit is not “one product” but “the amount of e-liquid it contains”.

Specifically, all products containing e-liquid are within scope, including:

Bottled e-liquid (whether containing nicotine or not)

Cartridges or pods containing liquid

Conversely, products without e-liquid are NOT subject to VPD – for example, empty devices (mods, battery sticks) and empty pods.

To summarise:

The UK is not taxing vaping hardware; it is taxing each millilitre of e-liquid.

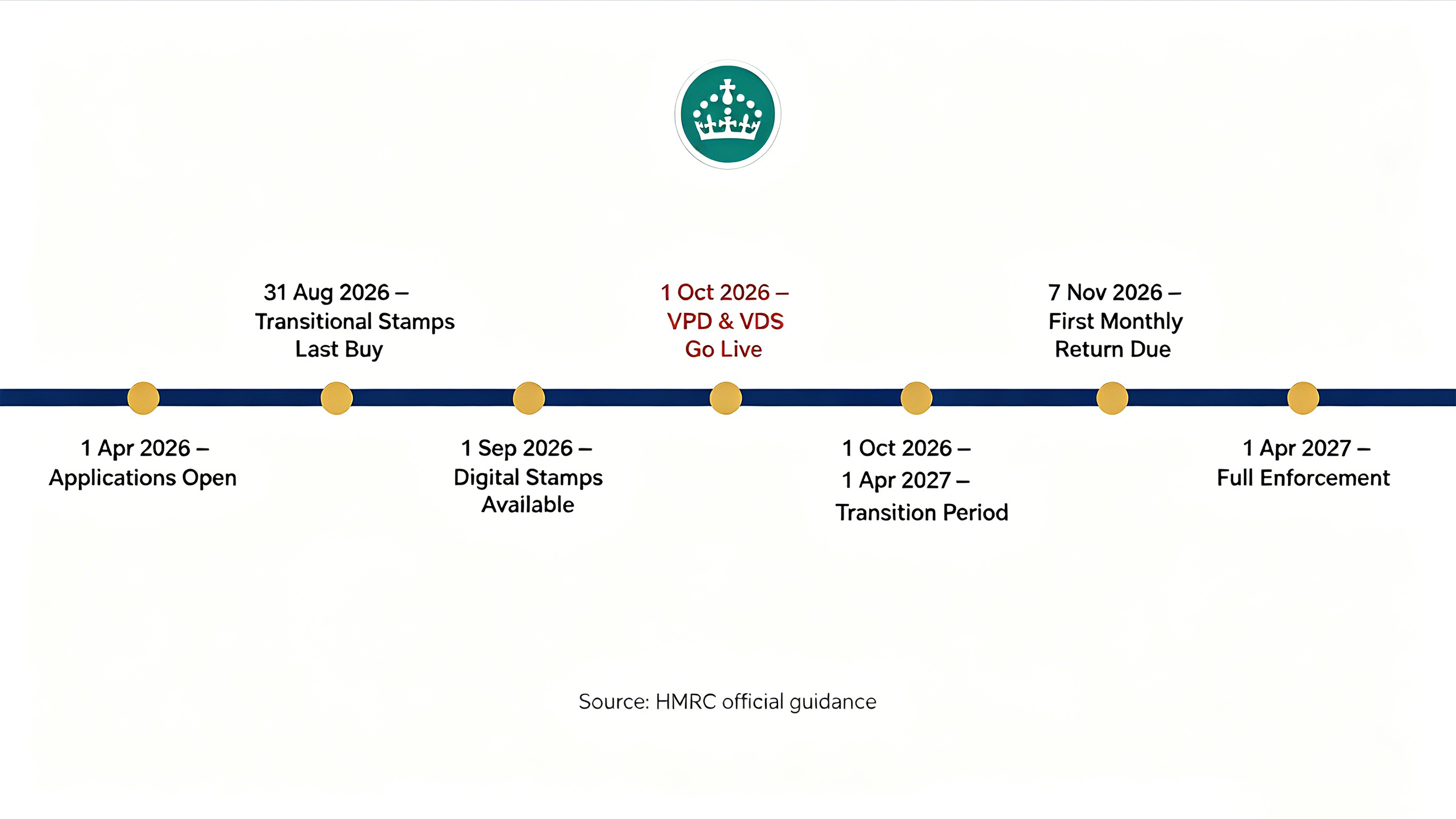

2. Key timeline

The UK has set out a clear implementation roadmap:

| Date | Key event |

|---|---|

| 1 April 2026 | Business registration applications open |

| 31 August 2026 | Last day to purchase transitional stamps (physical security only) |

| 1 September 2026 | Digital/scannable stamps become available for purchase |

| 1 October 2026 | VPD comes into effect; VDS duty stamp scheme starts. From this date, only digital stamps can be affixed |

| October 2026 – April 2027 | 6‑month transitional period – unstamped inventory can still be sold |

| 7 November 2026 | First monthly VPD return deadline |

| After 1 April 2027 | Full enforcement – all products must bear a duty stamp to be sold legally |

Additional notes:

Monthly VPD returns are due by the 15th of each month (next working day if non‑working day). A nil return is required even if no production or import took place that month.

Based on current processing times (HMRC recommends at least 45 working days), the closer you get to October, the longer and more uncertain the approval process. Brands should apply and adjust packaging structures as early as possible.

3. Duty rate & scope

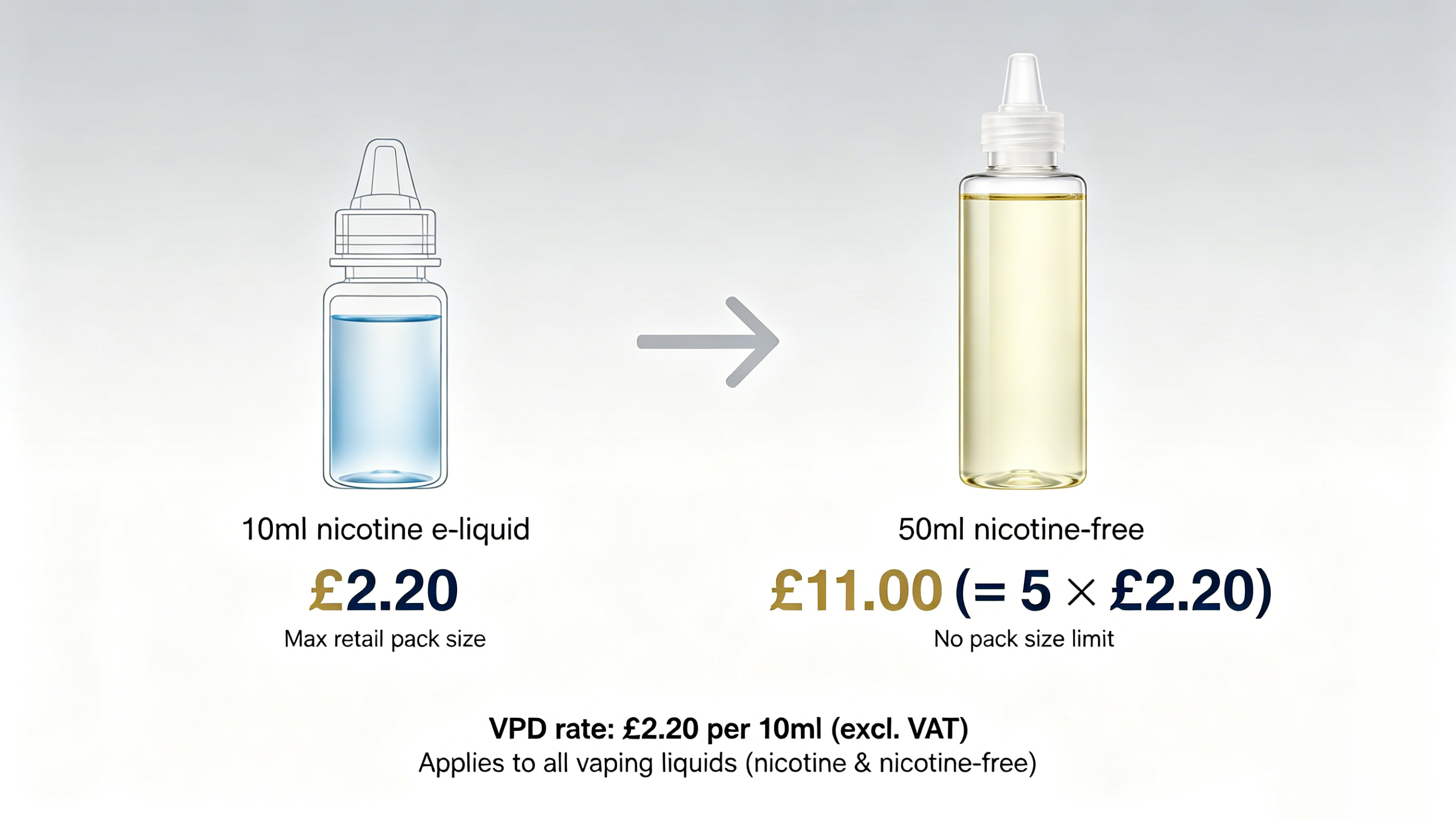

Duty rate: £2.20 per 10ml (excluding VAT)

Scope: All e-liquids intended for vaping, regardless of nicotine content, are taxed at the same rate.

Notes on volume:

Nicotine‑containing e‑liquids have a retail packaging limit of 10ml (under UK TRPR).

Nicotine‑free (0mg) e‑liquids have no packaging limit – VPD applies to the actual ml volume. For example, a 50ml 0mg e‑liquid would incur duty of £2.20 × 5 = £11.00.

This means that 0mg products, previously used by some to avoid regulation, are now also within the tax net – bringing the whole market under a unified tax framework.

4. Who needs to apply?

According to the latest HMRC guidance published on 1 April 2026, the following entities involved in relevant activities must submit an approval application to HMRC:

| Applicant type | Explanation |

|---|---|

| UK‑based brand/importer | Planning to import vaping products into the UK for sale |

| Overseas manufacturer (sending products directly to the UK) | Can apply through a UK representative who acts on their behalf and ensures compliance |

| UK‑based manufacturer | Manufacturing vaping products within the UK |

| Warehouse keeper | Managing a premises where unpaid duty vaping products are stored |

| Stamp processor | e.g., entities purchasing or affixing duty stamps |

Regardless of the route, approval must be held by a single legal entity – joint applications are not accepted.

5. What documents are needed for the application?

According to the official guidance, you must provide the following core information:

| Category | Details |

|---|---|

| Business info | Name, address, VAT or company tax reference (if any) |

| Responsible person | Name of one responsible individual |

| Premises plan | Showing security of production/storage areas, control of people and vehicle access |

| Business plan | Company structure, controllers, forecast production, import/export plans, and financial accounts (last tax year) |

| Estimated production | Total volume of e‑liquid expected to be produced in 12 months (in ml) |

| Stamp requirement | Number of stamps needed per 3‑month period (by different capacity sizes) |

| Financial guarantee | May be required for new businesses or those with tax compliance issues |

HMRC may carry out compliance checks at any time. If rules are not followed, approval will be revoked.

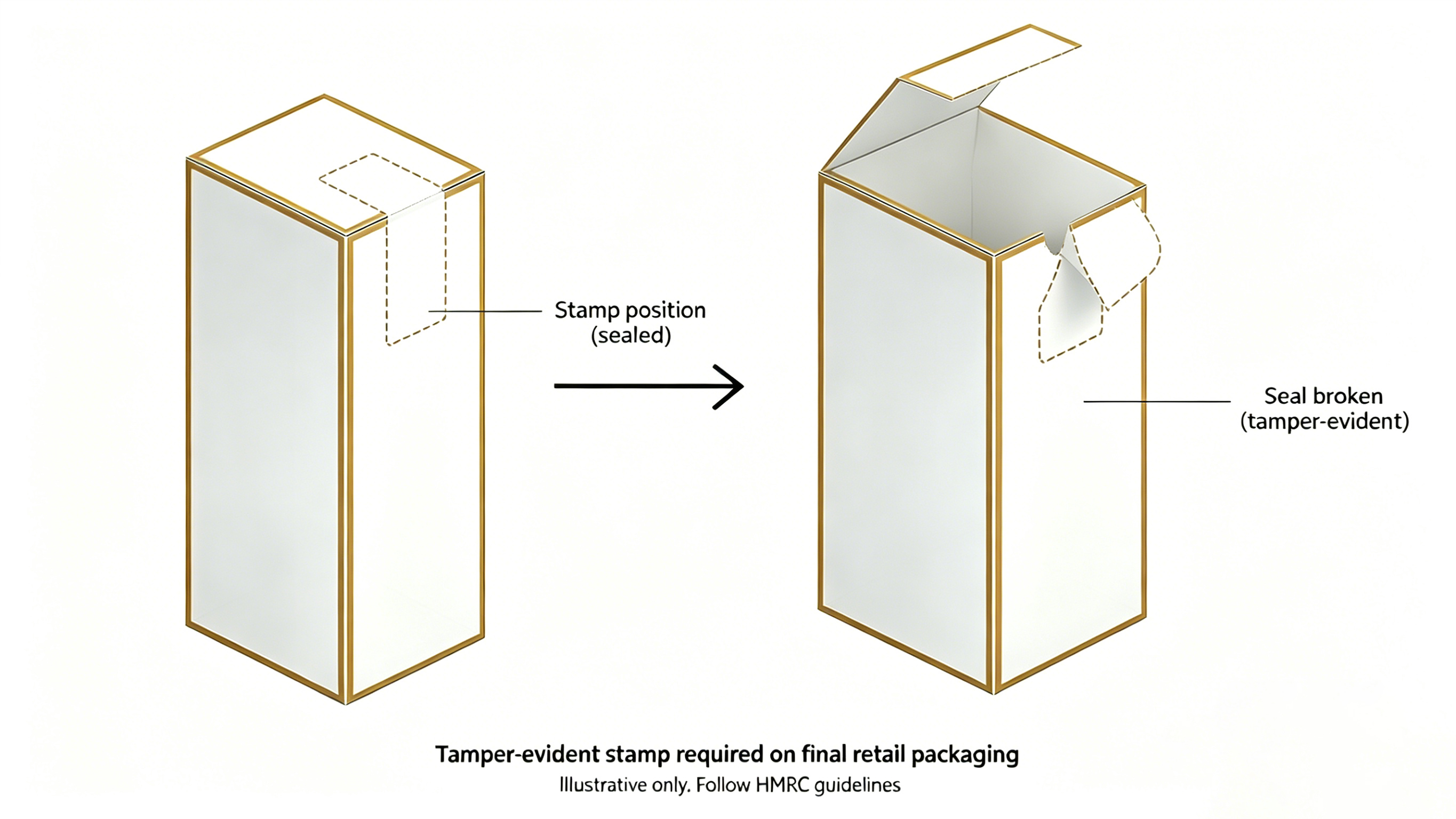

6. How should duty stamps be affixed?

HMRC has set out principle requirements rather than a detailed template.

Key requirements:

Stamps must have security features and a unique identification code for traceability and control.

They must be affixed to the final retail packaging.

They must be tamper‑evident – i.e., once the packaging is opened, the stamp must be irreversibly damaged.

Stamp specifications and ordering:

Size: 18mm × 42mm, rectangular

Minimum order: 1,000 stamps (wet glue or dry glue)

Standard wet glue pack: 20,000 stamps / roll (3‑inch core)

Cost: £14.47 per 1,000 stamps (excl. shipping; actual price as quoted by HMRC’s appointed supplier)

Appointed supplier: Cartor Security Printers Limited

For dry glue stamps, businesses must use an adhesive that ensures “opening = destruction” of the stamp.

Purchase limits and buffer:

HMRC sets a 3‑month rolling purchase limit based on declared production volume.

Certain overuse is allowed:

UK manufacturers/warehouse keepers: up to 30% over limit

UK representatives: up to 50% over limit

If no stamps are purchased for 36 consecutive months, approval will be revoked.

In practice, businesses can design their own stamp affixing method, as long as the tamper‑evident result is achieved.

⚠️ Important note: HMRC has not yet issued a unified diagram or standard template for stamp placement – only the result (cannot be opened without visible damage) is required. This means: the stamp issue is essentially a packaging design issue, not just a labelling issue.

Brands should discuss with their packaging suppliers and manufacturing partners early, reserve space for the stamp, and ensure the tamper‑evident effect.

7. Understanding the transitional period

A 6‑month transitional period runs from 1 October 2026 to 1 April 2027.

During this time, unstamped inventory already in the UK market can continue to be sold.

However, the purpose of this period is to clear existing stock, not to delay enforcement. New products entering the market must progressively switch to compliant versions. After the transitional period ends, all products on sale must have duty stamps affixed, otherwise they cannot be sold.

📍 Offline networking opportunity

We will be attending the Birmingham trade show from 8‑10 May 2026. Welcome to visit our booth for face‑to‑face discussions on VPD compliance, packaging adaptation solutions, and compliant product development.

To book an appointment or get our booth location, please contact us anytime.

📩 Contact YTOO: info@ytoojuice.com